The Ice Cream Vendor Who Discovered Financial Leverage – Simply Explained

This post tells the story of Raju, an ice cream vendor, who learns a crucial lesson about financial leverage. He realizes how to use borrowed money wisely to maximize profits. The post covers real-world applications of leverage, its risks, and when borrowing is a smart move.

Team Simply Explained

3/19/20254 min read

Imagine you run an ice cream cart. Life’s good, customers are happy, and you're making money. But one day, you realize you’re rejecting 100 customers daily because you run out of stock. That’s ₹500 in lost profits every single day! Frustrating, right?

What if you borrowed money, bought more stock, and sold to those extra customers? More sales, more profit! Seems like a brilliant plan—until it isn't.

Welcome to the world of financial leverage, where borrowing money can multiply your gains or crush you under debt. Let’s break it down using our ice cream hero, Raju.

Raju’s Grand Plan (and Where It Went Wrong)

Meet Raju, the Ice Cream Vendor

Raju sells ice creams from his cart every day. He buys them from a dealer at ₹10 per unit and sells them at ₹15 per unit. He purchases 100 ice creams daily, making a total profit of ₹500.

But there’s a problem. He consistently runs out of stock and turns away 100 potential customers daily. That’s another ₹500 he could have earned! But he doesn’t have enough money to buy more stock.

One day, Raju has an idea: “What if I borrow money, buy more ice cream, and make more profit?”

Deal with Mohan

Raju pitches the idea to his friend Mohan, asking for ₹1000 to buy 200 ice creams instead of 100. Mohan agrees—but on one condition: he wants a share of the profit equal to his capital contribution.

Raju, excited by the idea of selling double the ice creams, agrees.

The Shocking Outcome

With ₹2000, Raju buys 200 ice creams.

He sells all of them and makes ₹3000.

He shares the profit equally with Mohan since they both contributed ₹1000 each.

Each gets ₹1500.

Raju realizes something terrible: he is making the same ₹1500 as before, even after doubling his effort!

That’s when frustration kicks in. Raju worked twice as hard but made zero extra money for himself.

So, what happened?

Raju’s Wife Saves the Day

Raju had always known that his wife was smart. She managed their household expenses with ease, ensuring every rupee was spent wisely.

Frustrated with his financial situation, Raju came home one evening and told his wife about his failed plan. “I borrowed money, doubled my stock, worked twice as hard, and yet… I didn’t make any extra profit!” he sighed.

His wife smiled knowingly. “Sit down, Raju,” she said, pulling out a small notebook. “Let’s look at the numbers.” and then explains where he went wrong

“Mohan made you share the profits in the same ratio as capital investment. That means he became your silent partner—not just a lender. You’re doing all the work, but he’s taking half the profits without lifting a finger.”

She continues:

“If you had borrowed money at a fixed interest rate instead of sharing profits, you would have actually made more money.”

And just like that, Raju learns the secret to financial leverage.

The Secret to Smart Borrowing (Leverage Done Right)

Raju’s mistake? He gave away profits in proportion to the borrowed amount, treating Mohan like a business partner instead of a lender.

Here’s the Right Way to Use Leverage:

✅ Borrow at a fixed interest rate, not a revenue share.

✅ Ensure your return on capital is higher than the cost of borrowing.

✅ Never give equal profit share for borrowed money (unless you want a partner, not a lender).

Let’s fix Raju’s deal. This time, Mohan lends ₹1000 at 10% interest instead of demanding half the profit.

How It Works Now:

Raju buys 200 ice creams (₹2000).

Sells all for ₹3000.

Pays back ₹1100 (₹1000 + ₹100 interest).

Keeps the remaining ₹1900.

Instead of the ₹1500 earlier, he now earns ₹1900 on his ₹1000—a 90% return! That’s leverage done right.

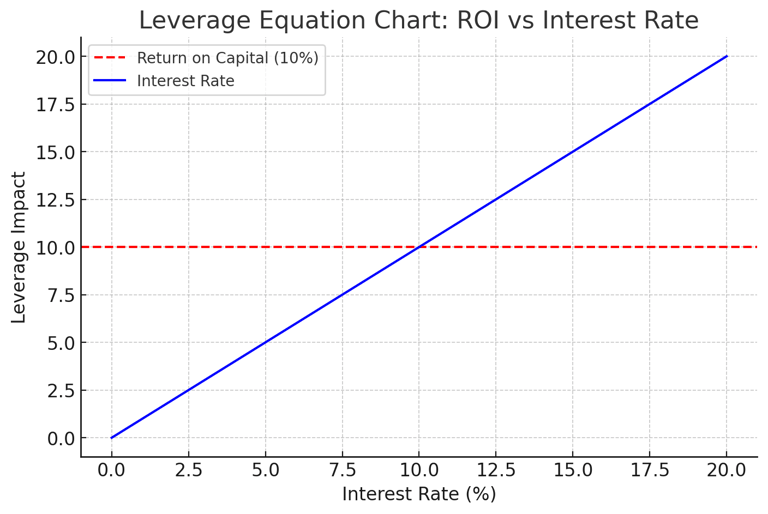

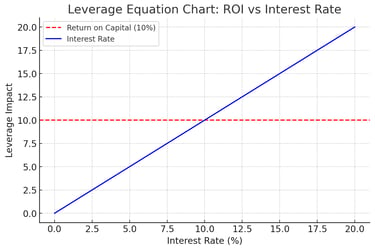

Simple Rule of Financial Leverage

📌 If Return on Capital > Interest Rate, borrowing is a great idea.

📌 If Return on Capital <= Interest Rate, borrowing is pointless or risky.

For example:

If the loan interest was 60%, Raju would owe ₹1600, leaving him with only ₹1400—a bad deal.

The higher the cost of borrowing, the less leverage benefits you.

Here is the Leverage Equation Chart, illustrating the key rule:

✅ If Return on Capital (10%) > Interest Rate, borrowing is beneficial.

❌ If Return on Capital ≤ Interest Rate, borrowing is risky.

Real-World Leverage: Beyond Ice Cream

Where Leverage Works Well:

✅ Real Estate: A person buys a property worth ₹50 lakh but only pays ₹5 lakh upfront (10% down payment) by taking a loan for the remaining ₹45 lakh. They have to pay monthly EMIs, which include both interest and principal repayment. If property prices rise by 10%, the house is now worth ₹55 lakh. After repaying part of the loan through EMIs, they still make a profit due to leverage. However, if property values fall or EMI payments become unmanageable, the risk increases.

✅ Businesses: Companies borrow money to open new locations, invest in equipment, or expand operations. If revenues grow faster than borrowing costs, profits increase.

✅ Stock Market: Investors use margin (borrowed money) to buy more stocks than they could with their own money. If stock prices go up, they earn higher returns than if they had invested only their own funds.

Where Leverage is Dangerous:

❌ High-Risk Stock Trading: Using borrowed money to trade stocks or crypto can result in major losses if prices drop suddenly.

❌ Excessive Business Debt: If a company takes on too much debt and cannot generate enough revenue, it may face bankruptcy.

❌ Personal Debt Traps: Credit cards and personal loans with high-interest rates can quickly spiral out of control, making it difficult to repay the borrowed amount.

Final Takeaway: Use Leverage Wisely

Financial leverage is like a sharp knife—use it well, and it makes life easier; use it wrong, and it cuts deep.

If Return on Capital > Interest Rate, leverage is a wealth-building tool. If not, it’s a debt trap. Be like Raju (the second time, not the first), and make borrowing work for you!

Insights

Weekly blogs simplifying various intriguing topics.

Connect

Explore

contact@simplyexplained.com

Copyright © 2025 Simply Explained Powered by DigiPar